Central bankers like to focus on core inflation readings, which strip out food and energy prices, but that doesn’t mean that they, or investors, will be able to ignore a renewed surge in crude-oil prices.

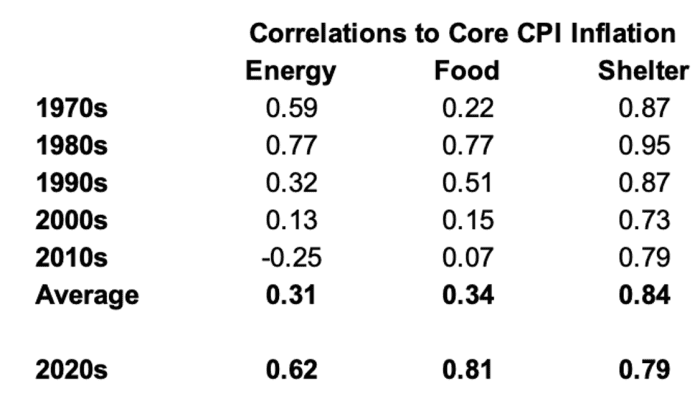

In a Thursday note, DataTrek Research observed that the correlation between energy prices and the core reading of the consumer-price index has returned to levels seen in the 1970s and 1980s. It stands at 0.62 since 2020, compared with an average of 0.68 in those prior decades, and well above its long-run average of 0.31. A reading of 1.0 would mean the measures were moving in perfect lockstep. (See table below.)

Core measures of inflation typically strip out volatile items like food and energy. While that often leads to eye-rolling by commentators who note that food and energy make up a big chunk of what consumers spend money on, the logic behind the move holds that such items are less responsive to monetary policy.

Policy makers put more emphasis on the core reading for a better read on what they can influence. The core personal-consumption expenditures, or PCE, index, for example, is often described as the Federal Reserve’s favored inflation indicator.

But that doesn’t mean rising energy or food prices can be ignored. Energy, after all, is an input, and can have an influence on overall prices.

“Recent data says energy prices hold more sway on core inflation than any time since the 1970s/1980s, so rising oil prices are a legitimate concern for both the Fed and capital markets. Food inflation fits the same bill,” said DataTrek co-founder Nicholas Colas in the note.

Oil prices have been on a tear this summer, with the rally accelerating after Saudi Arabia announced earlier this week it would extend a production cut of 1 million barrels a day through the end of the year, with Russia also pledging to extend a supply cut.

West Texas Intermediate crude

CL00,

The surge in crude threatens to further drive up fuel prices, including gasoline and diesel.

And rising oil prices this week got a chunk of the blame from investors and analysts for a pickup in Treasury yields as market participants began to pencil in a longer stretch of higher interest rates — or weighed the possibility the Fed may need to deliver more monetary tightening. That’s also contributed to a rise in the U.S. dollar, with the ICE U.S. Dollar Index DXY, a measure of the currency against a basket of six major rivals, hitting a six-month high.

U.S. stocks have weakened in the face of rising yields, with technology and growth shares, which are particularly rate-sensitive, leading the way lower. The Nasdaq Composite COMP was on track for a 2% decline so far this holiday-shortened week, while the S&P 500 SPX has pulled back 1.4% and the Dow Jones Industrial Average DJIA has lost 1%.

“With oil prices rising again, we got to wondering about the spillover effects of this move on inflation. Will pricier crude derail recent disinflationary trends?” Colas wrote.